Dale Brunk, CEBS, AIF®

Are you in your early sixties and hoping to make a splash in your retirement strategy? The SECURE Act 2.0 introduced a $11,250 catch-up contribution for those aged 60-63.

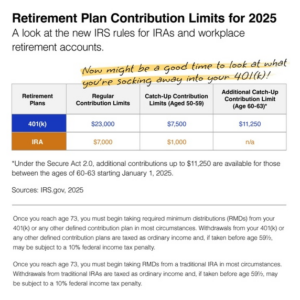

Catch-Up Contributions

This “super catch-up” is part of a new tiered catch-up contribution for workers participating in 401(k), 403(b), governmental 457 plans, and the federal government’s Thrift Savings Plan. This follows SECURE Act 2.0’s revised age for Required Minimum Distributions (RMD) and expanded access to 401(k) plans for part-time employees. With these higher contributions, you might be able to lower your taxable income.

Contribution Limits

The base annual contribution limit for these accounts has gone up to $23,500, up from $23,000 in recent years.1

For regular Individual Retirement Accounts (IRAs), the contribution limit remains unchanged at $7,000, with an additional $1,000 contribution available for those over age 50.1

For workplace retirement accounts, like the 401(k), the catch-up contribution for those over 50 remains the same at $7,500 for 2025.1

The higher contribution level supersedes the 50+ catch-up; unfortunately, you won’t be able to do both! The chart below outlines the 2025 limits.1

For those who participate in workplace plans, this offers an opportunity to reevaluate their contributions and potentially invest more money into their retirement strategy. If that sounds like a good idea to you, let’s have a conversation about this soon.1.

IRS, November 12, 2024